India has just rolled out GST 2.0, its most sweeping Goods and Services Tax overhaul since 2017. The 56th GST Council meeting approved a simpler two-slab structure—5% and 18%—plus a special 40% “de-merit” rate for a narrow set of luxury and sin goods. Most changes kick in September 22, 2025 (Navratri Day 1). Tobacco and related items will transition later, on dates to be notified. (Reuters, EY, The Times of India)

Beyond rates, the Council also pushed important ease-of-doing-business fixes—like operationalizing the GSTAT (appeals), clarifying intermediary services (place of supply to recipient, aiding exports), and enabling risk-based provisional refunds, especially for zero-rated and inverted duty cases. These matter for cash flow and litigation reduction across sectors. (EY)

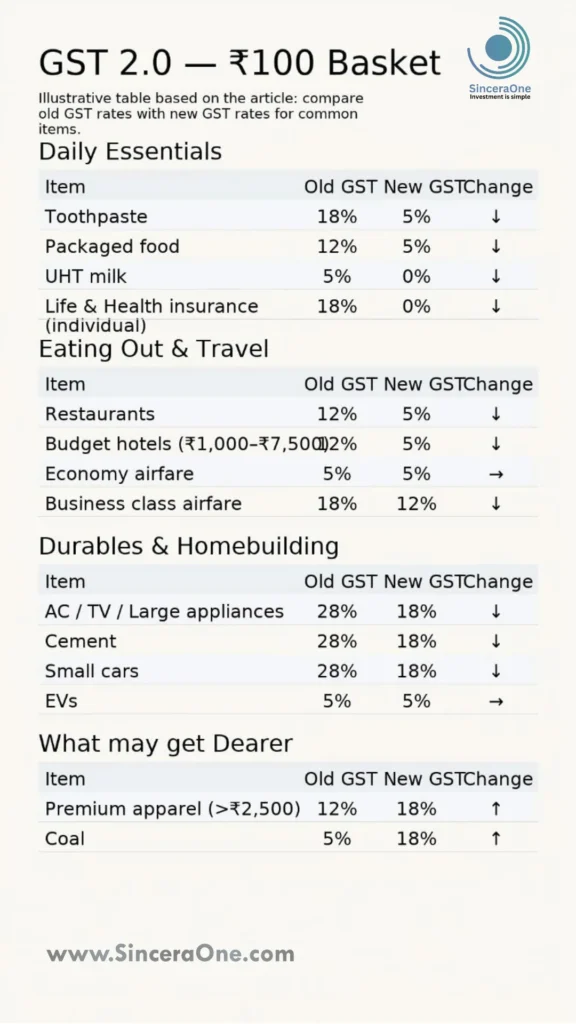

What’s changing in your daily cart with GST 2.0

The practical question for households: what gets cheaper, what doesn’t, and what’s exempt?

- Essentials: Items of everyday use like packaged foods, toothpaste, milk products slide to 5% (from 12–18% earlier), while UHT milk joins other dairy in nil GST—ending the oddity where only UHT was taxed. Life and health insurance premiums for individuals are tax-free—a big wallet win. (Reuters, The Times of India, www.ndtv.com)

- Eating out & travel: Industry trackers highlight restaurants moving to 5% (from 12–18% ranges) and budget hotel rooms (₹1,000–₹7,500) down to 5% (from 12%). Economy airfares remain at 5% while business class drops to 12%—good news for festive travel. (Navbharat Times, www.ndtv.com)

- Consumer durables: TVs, ACs, dishwashers, large appliances—and crucially, many cars—shift down to 18% from 28%, priming a festive-season demand bump. EVs remain at 5%. Mid-to-large cars move to an effective 40% without additional cesses, down from ~50%. (Reuters)

- Construction basket: The long-anticipated cut in cement—from 28% to 18%—is here, easing project costs and potentially per-sq-ft prices (depending on pass-through). Developers and homebuyers stand to benefit. (Business Standard, Hindustan Times)

- What may get dearer: Apparel above ₹2,500 climbs to 18% (from 12%), a pinch for premium retail. Coal moves to 18% (from 5%), lifting input costs in energy-linked value chains. Fizzy drinks stay effectively at 40%. (Reuters)

Inflation angle: If reductions are fully passed through, economists see headline CPI easing by up to ~1.1 percentage points, cushioning households and improving real purchasing power. (Reuters)

Who gains (and who doesn’t): sector-by-sector

FMCG & Retail: Lower GST on soaps, shampoos, toothpaste, packaged food, and basic personal care can expand volumes and aid premiumization in mass segments. Expect tailwinds for consumer names (HUL, Nestlé, Godrej et al.) as pricing power meets pent-up festive demand. (Reuters)

Autos & Mobility: Bringing small cars to 18% and simplifying the levy on bigger vehicles (effective 40% without layered cesses) cleanly refactors pricing ladders. Add the steady 5% on EVs, and the sector enters Q3 with a demand-friendly tax curve. Ancillaries (tyres, select auto parts) tied to cuts also benefit. (Reuters)

Consumer Durables & Electronics: Big-ticket purchases—TVs, ACs, white goods—head into peak season cheaper, which could lift footfalls, conversion rates, and average ticket sizes for retailers and OEMs. (Reuters)

Real Estate & Materials: Cement at 18% is a structural cut. Analysts expect 5–7% project cost savings in some builds, improved viability for affordable housing, and faster site mobilization—subject to how quickly input suppliers pass on benefits. Granite/marble and construction inputs getting relief further de-stress budgets. (The Economic Times, The Times of India)

Textiles: Two divergent forces:

- Relief on man-made fibre/yarn (inversion fix towards 5%) can improve export competitiveness and working capital.

- Higher GST on premium apparel (>₹2,500) to 18% may weigh on discretionary fashion.

Net-net, basics and exports look better; premium retail has to recalibrate. (Press Information Bureau, Reuters)

Energy & Metals: Coal at 18% raises an input line; watch margin management downstream. Chemical/fibre inputs see relief elsewhere, indicating a calibrated approach to input costs. (Reuters, The Indian Express)

Insurance & Healthcare: Individual life/health insurance exemptions meaningfully improve affordability and can deepen protection penetration. Healthcare devices and essentials seeing reductions add incremental relief for households. (Reuters)

GST 2.0 & Markets: the early read

The first reaction was constructive. Nifty and Sensex opened firmer, with auto and consumer stocks leading—logical, given the immediate demand stimulus. Energy lagged on select oil-linked tax tweaks. Traders note the “good news” was partly priced in, but the consumption impulse and compliance simplification remain supportive for earnings stability into H2 FY26. (Reuters)

Broker commentary is converging on three themes:

- Lower costs + simpler slabs → cleaner forecasting for CFOs, better capex visibility.

- Consumption kicker ahead of festivals could widen breadth in mid-cap consumer names.

- Watch implementation (IT systems, open-stock ITC, revised pricing) to gauge how much of the macro boost translates to margins vs. price cuts. (mint)

The long-term picture: simpler, fairer, more growth-friendly—if executed well

- Simplicity & compliance: Two core slabs reduce classification disputes and compliance complexity. Expect fewer “rate-fitment” ambiguities and smoother audits. GSTAT and clarified intermediary rules should reduce litigation tail-risk. (EY)

- Inflation & demand: With headline CPI likely softer if pass-through is robust, discretionary spending can broaden beyond metros—helpful for FMCG, durables, and housing. (Reuters)

- State finances & Centre’s math: The Centre pegs revenue foregone at ~₹48,000 crore, smaller than bearish forecasts—banking on volume growth, compliance gains, and buoyant direct taxes to bridge. Monitor monthly GST collections for proof. (Reuters)

- Industry fixes: Tackling inverted duty (textiles, renewables, agri machinery, etc.) enhances competitiveness and unclogs refunds—vital for MSMEs. Provisional refunds (risk-based) can ease working capital strain if implemented tightly. (EY)

- Risks to watch: Transition frictions (billing/ERP changes by Sept 22), pricing playbooks (retail MRPs vs. input credits), and sectors facing hikes (premium apparel, coal-linked value chains). A fair amount hinges on how much benefit is passed to the consumer and how quickly.