Imagine walking into a store to buy a raincoat. You ask for something that protects you from the rain. The salesperson hands you a fancy jacket that looks great but barely repels water. It’s expensive, hard to return, and comes with a bunch of hidden charges. You walk out thinking you’ve bought protection—but what you really got was a fashion item with poor functionality.

That’s exactly what’s happening in India’s insurance industry today.

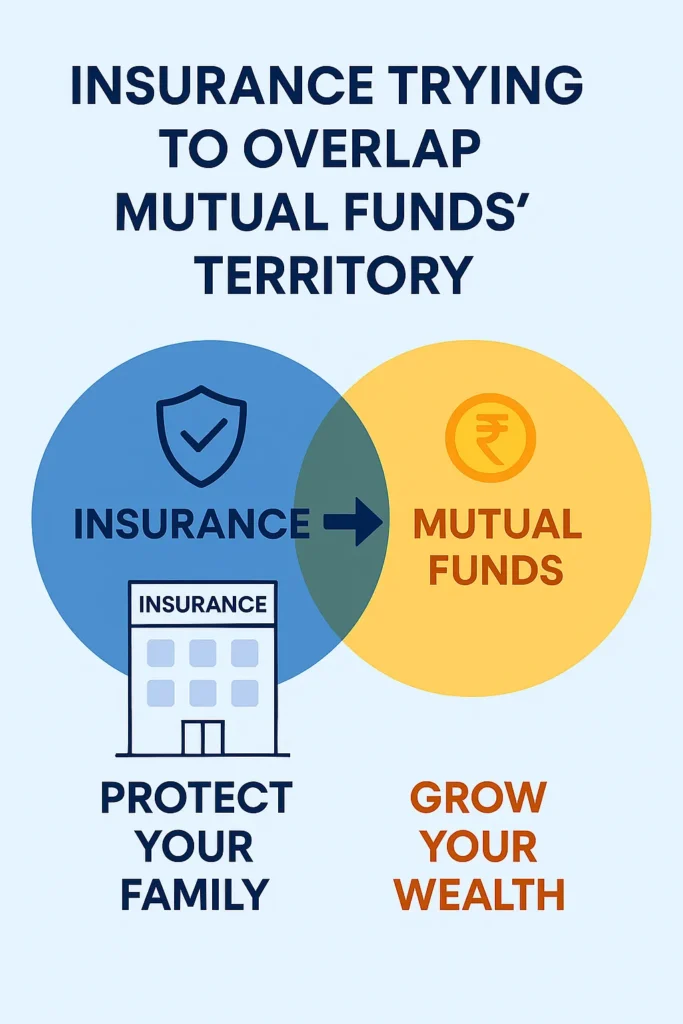

The Hidden Truth About Insurance Products

Most people buy insurance thinking they’re securing their future. But what they often end up with are investment products disguised as insurance—like ULIPs (Unit Linked Insurance Plans) and traditional endowment policies. These products promise returns, protection, and tax benefits. But here’s the catch: they’re opaque, expensive, and inflexible.

Let’s break it down.

- ULIPs invest your money in market-linked funds, but you rarely know where your money is going.

- Endowment policies offer guaranteed returns, but those returns are often lower than inflation.

- Both come with complex charges—mortality fees, fund management fees, policy admin charges—and lock you in for years, making it hard to exit without losing money.

Compare this to a mutual fund SIP:

- You know exactly what you’re investing in.

- You can exit anytime after a short lock-in.

- Charges are transparent and regulated.

So why do insurance companies push these products so hard?

The Business Model That Works Against You

Here’s the uncomfortable truth: the insurance industry isn’t just about protection anymore. It’s become a high-cost investment business that thrives on regulatory loopholes.

Insurance companies—often owned by banks—run mutual fund businesses that are transparent and investor-friendly. But when they sell investment products through their insurance arms, they abandon those principles. Why? Because insurance regulations are outdated and allow practices that would be illegal in the mutual fund space.

This is called regulatory arbitrage—exploiting the gap between two sets of rules to maximize profits.

And it’s not just the companies. Even well-meaning insurance agents are caught in this trap. Selling term insurance (which actually protects you) earns them peanuts. But selling ULIPs or endowment plans? That’s where the big commissions lie.

So even if an agent wants to do right by you, the system nudges them toward products that serve you poorly.

Real-Life Example: Raj’s Costly Mistake

Raj, a 35-year-old professional, wanted life insurance. His agent sold him a ULIP, saying it’s “insurance plus investment.” Raj paid ₹50,000 annually for 10 years. At the end of the term, his fund value was ₹5.8 lakh—barely more than what he paid. Had he bought a ₹1 crore term plan for ₹8,000/year and invested the rest in a mutual fund SIP, he’d have had ₹12–15 lakh instead.

Raj didn’t just lose money—he lost time, flexibility, and protection.

So What Can You Do?

Let’s flip the script. Here are five practical ways to protect yourself and make smarter choices:

1. Buy Pure Term Insurance First

Term plans are the only true insurance products. They’re cheap, simple, and offer high coverage. For example:

- A 30-year-old non-smoker can get ₹1 crore coverage for ₹8,000–₹10,000/year.

👉 If you don’t have term insurance yet, make it your first priority. Use platforms like Policybazaar or InsuranceDekho to compare plans , alternatively you can contact us to buy transparent insurance policy

2. Separate Insurance from Investment

Don’t mix protection with wealth creation. Instead:

- Buy term insurance for security.

- Invest in mutual fund SIPs for growth.

Example:

- ₹10,000/month in a SIP for 20 years can grow to ₹75–80 lakh.

- Combine that with a ₹1 crore term plan and you’re truly covered.

👉 Use SIP calculators to visualize your future wealth. Start small, but start now.

3. Ask for Commission Disclosure

Before buying any insurance product, ask your advisor:

- “How much commission do you earn from this?”

- “Is there a better alternative for me?”

This builds trust and helps you spot misaligned incentives.

👉 Demand transparency. If your advisor hesitates, consider switching to a fee-only planner.

4. Use Digital Dashboards

Choose platforms that offer:

- Real-time fund performance

- Clear breakdown of charges

- Easy exit options

👉 If your insurer doesn’t offer this, ask why. Or move to one that does.

5. Educate Yourself and Others

The more you know, the better you choose. Follow blogs, attend webinars, and read product fact sheets.

👉 Share this article with friends and family. Help them avoid costly mistakes.

What Regulators Must Do

While individual action matters, systemic change is essential. Regulators like IRDAI must:

- Mandate mutual fund-style disclosures for ULIPs and endowment plans.

- Cap charges and commissions.

- Promote term insurance as the default product.

Until then, consumers must stay vigilant.

Final Thoughts: Don’t Be a Passive Buyer

Insurance is supposed to protect you—not trap you. The current system thrives on confusion, complexity, and misplaced trust. But you have the power to change that.

Ask questions. Compare products. Demand clarity.

Because when you buy insurance, you’re not just spending money—you’re making a bet on your future. Make sure it’s a smart one.

Ready to take control? Start by reviewing your current policies. If they’re not serving you, it’s time to rethink.

Share This Message

If this article helped you see things differently, share it. Let’s build a community of informed, empowered insurance buyers.