What is the e-Rupee?

Imagine you give your younger sibling ₹500 each month for pocket money—but you only want them to spend it on lunch at school, not on video games or toys. With the programmable e-Rupee, you can “lock” those ₹500 so they only work at the school cafeteria.

Here’s how it works step by step:

- You or a program (like your school’s finance office) creates a batch of digital rupees and tags them with a rule:

– “Can be spent only at Merchant IDs registered as ‘school cafeteria’.”

– “Expires if not used by the last day of the month.” - Your sibling’s e-Rupee wallet receives exactly ₹500 with those tags attached.

- When they tap or scan to pay for a sandwich, the system checks the rule, sees “OK to spend here,” and completes the purchase instantly.

- If they try to buy a comic book at another shop, the payment is declined—because the rule doesn’t allow it.

Why It Matters

- Fraud protection: Money can’t leak out to unauthorized sellers.

- Targeted support: Schools or governments can send subsidies that only pay for books, meals, or medicines.

- Automation: No manual tracking of how money is used—rules are enforced by the digital currency itself.

Everyday Example

A city council wants to help low-income families buy fresh produce but not soda or snacks. They issue each eligible household ₹1,000 in programmable e-Rupees tagged for “vegetable vendors only.” Families simply scan their e-Rupee wallet at approved markets and get their veggies—guaranteed.

In a nutshell, programmable e-Rupee turns regular money into “smart money” that follows your rules automatically making targeted payments easier, safer, and more efficient.

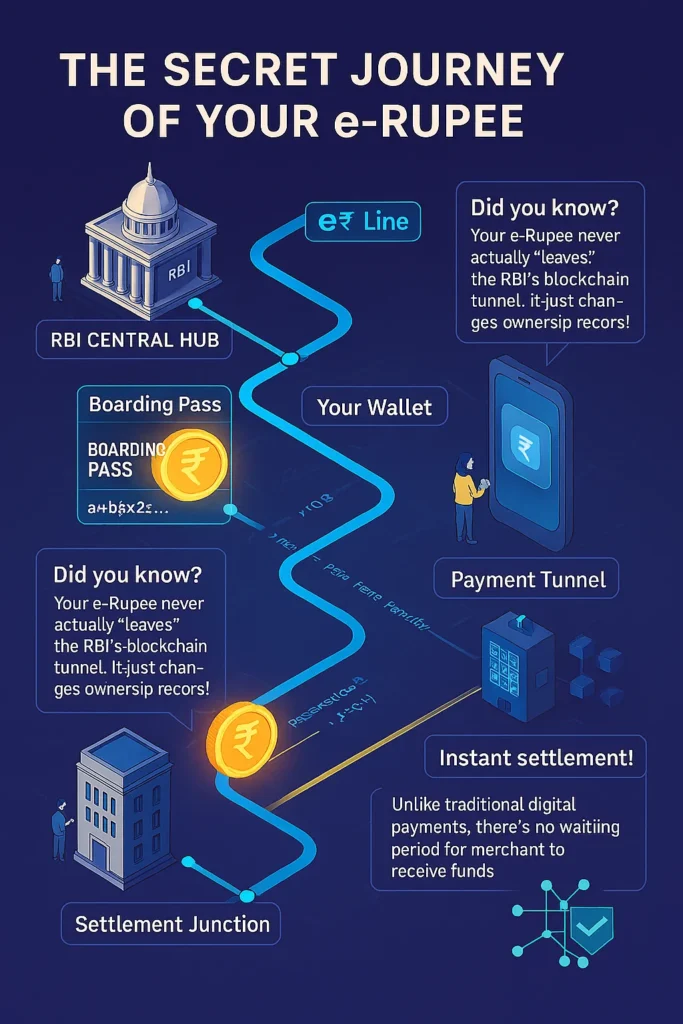

Think of the e-Rupee as digital cash issued by India’s central bank. Just like the notes in your pocket, it’s a legal way to pay for things. The big difference is that it lives on your phone or a special digital wallet. You can use it anywhere regular rupees are accepted—online or in person.

For example, if you buy tea at a roadside stall, you could scan a QR code and pay with your e-Rupee instead of handing over cash.

How Does It Work?

Under the hood, the e-Rupee runs on a two-tier system:

- RBI Core

The Reserve Bank of India (RBI) creates and tracks the total amount of e-Rupee in circulation. - Banks and Service Providers

Your bank or a payment app gives you a digital wallet. They handle sign-ups, KYC checks, and day-to-day customer support.

When you pay someone, the e-Rupee moves from your wallet to theirs, with the RBI updating its records in the background.

Key Features with Everyday Examples

- Offline Payments

Imagine you’re at a village fair with no internet. You can still tap or use Bluetooth to transfer e-Rupees. Once you’re back online, your wallet syncs all the transactions. - Programmable Money

Think of sending pocket money to your child but only for books and school fees. Programmability lets the giver set rules on how funds are used. - Instant Finality

Unlike UPI transfers that might take a few seconds, e-Rupee payments settle instantly—no chance of “payment pending.”

Top Practical Uses

1. Daily Purchases (P2M and P2P)

Pay your friend back for movie tickets or buy groceries at a kirana store. Since there’s no middleman fee, merchants don’t pay extra charges.

2. Government Benefits (G2P)

Suppose the government sends you a health subsidy. With e-Rupee, they can tag that money only for doctor visits or medicines. It cuts down on leaks and ensures funds reach the right people.

3. Public Transport and Toll Booths

Picture tapping your phone on the metro gate or toll plaza and walking through in seconds, even if you’re paying just ₹5. No change, no queue.

4. Small Shops and Rural Markets

Street vendors can accept digital payments on basic phones. This helps shop owners in small towns go cashless without internet problems.

Challenges to Watch Out For

- Privacy vs. Rules

People like cash for privacy, but regulators need records to fight fraud and money laundering. Balancing both is tricky. - Keeping It Secure

Digital wallets and phones can be hacked. The system must use strong security—like encrypted keys stored in secure hardware. - Avoiding Double-Spends Offline

If you pay someone offline, there’s a tiny risk you might try to spend the same e-Rupee twice. Wallets need smart checks to stop that. - Not Hurting Banks

If everyone moves money into e-Rupee wallets, banks could lose customer deposits. RBI can set holding limits or keep the digital currency non-interest bearing to ease this.

How It Impacts Society and Money

- Better Financial Inclusion

People without bank accounts can still join the digital economy. Even low-KYC wallets let them make small payments. - Lower Cash Costs

The government spends billions printing and transporting notes. Digital cash cuts these costs and reduces counterfeit notes. - Faster Welfare Delivery

Instant, tagged transfers mean subsidies and benefits arrive and get used immediately, without middlemen. - Boosting Trust

Central-bank-backed digital money builds confidence. You know there’s no risk of an app shutting down and your balance disappearing.

Big-Picture Economic Effects

- New Business Ideas

Programmable money can power pay-per-use services, like paying for electricity by the minute or releasing funds only when tasks are done. - Sharper Policy Tools

RBI can see real-time payment flows and tailor interest rates or liquidity measures quickly during emergencies. - Safer Wholesale Markets

Banks can settle between themselves instantly, reducing the risk of one party defaulting on a large trade. - Formalizing the Economy

More digital payments mean a clearer paper trail, which helps expand the tax base and unlocks easier loans for small businesses.

How It Could Reshape India’s Economy

- Cash-Like Convenience, Digital-Age Speed

Anywhere you carry your phone, you carry money you can use offline. No network? No problem. - Targeted Public Spending

Subsidies and grants get locked for specific uses and timelines, cutting waste and fraud. - Empowering MSMEs

Small traders can offer flexible payment terms—like paying suppliers when goods arrive—through smart contracts. - Global Money Flows

In the future, e-Rupee corridors with other countries could make remittances faster and cheaper.

Simple Steps for Businesses

- Add e-Rupee acceptance alongside UPI on your existing QR codes.

- Pilot programmable payouts—like escrow for customer refunds.

- Design for offline use by adding sync reminders and showing clear limits.

- Embed compliance controls—set transaction caps and real-time fraud alerts.

By keeping it simple and customer-friendly, businesses can get ready for the e-Rupee wave and help drive India’s digital economy forward.